abstract

A deal between the USA and China appears shut, which might see markets rethink their extremely-cautious expectations on US imperative financial institution policy.

issues about international increase may delivery to fade too.

in the meantime, the probability of a 'no deal' Brexit, and tariffs on eu automobiles, means uncertainty will continue to be high.

at first posted March eight, 2019via Mark Cliffe, Chief Economist

March is shaping up to be a huge month for geopolitics. A deal between the united states and China seem shut, which could see financial markets rethink their ultra-cautious expectations on US significant bank policy. concerns about world growth might delivery to fade too. That stated, a handful of obstacles could yet supper a US-China deal. in the meantime, the chance of a 'no deal' Brexit, and tariffs on ecu vehicles, suggest the uncertainty facing policymakers and buyers will stay high.

The Federal Reserve has adopted a greater cautious method to fiscal coverage considering the beginning of the yr. alternate tensions, the turmoil in fairness markets and tighter financial situations are noted as 'go-currents' which are growing uncertainty, and in an ambiance of low inflation, the Fed can have enough money to be 'patient'.

although, these tensions look like easing. Borrowing charges have fallen again, equities have recovered all their losses, and there are nice indications involving a possible US-China change deal. With the jobs market roaring forward, higher pay and rising inflation pressures imply that there is a strong case for a summer time activity cost upward push. This remains at odds with fiscal markets, which might be pricing in a protracted pause with an eventual expense cut in 2021.

Sentiment symptoms have begun to stabilise in the eurozone having normally declined due to the fact that the start of 2018. besides the fact that children, any rebound looks to stay muted as a exchange battle with the U.S. and a chaotic Brexit remain large dangers, maintaining uncertainty excessive. What's greater, core inflation has fallen back below 1%, nipping any expectation of monetary tightening within the bud. basically, the ECB has now extended its forward counsel of stable rates as much as the end of 2019 and has also announced a new collection of TLTROs to steer clear of a tightening in credit situations.

the united kingdom top Minister faces an uphill combat to get her deal authorised by Parliament, despite pointers that her opponents may be transferring their place. That skill an extension to the Article 50 negotiating length now looks inevitable, but if this delay is kept distinctly short, the threat of 'no deal' will remain. so that it will keep the power on the financial system, further reducing the chances of a fee hike this 12 months.

China's executive has supplied a collection of aims for 2019. nearly every thing was as anticipated, chiefly the new GDP growth goal. The government is relying much more on fiscal stimulus in preference to monetary easing. A repeat of previous assistance on the trade fee mechanism may additionally mean the yuan will proceed to observe the greenback index.

the 10-year German yield at a mere c.20 basis features bears no reflection on the Germany economic climate. So how can we make feel of this? To maintain it undeniable and straightforward, it's a measure of concern. That worry is a combination of two aspects. First, there's the 'macro' worry that the current slowdown could turn into extra severe. however by means of a ways essentially the most large point is an existential fear about the European challenge itself, and never satisfactory consideration is being paid to this. The ecu elections in may additionally may show pivotal.

In FX, we proceed to look for additional USD outperformance vs the low yielding G10 currencies in coming months. The Fed will carry a hike, whereas the likes of ECB or BoJ will remain dovish /neutral. The period of the Article 50 extension will count number for GBP cost motion, with longer extension being extra effective for GBP than shorter. within the CEE FX space, our excellent select remains HUF.

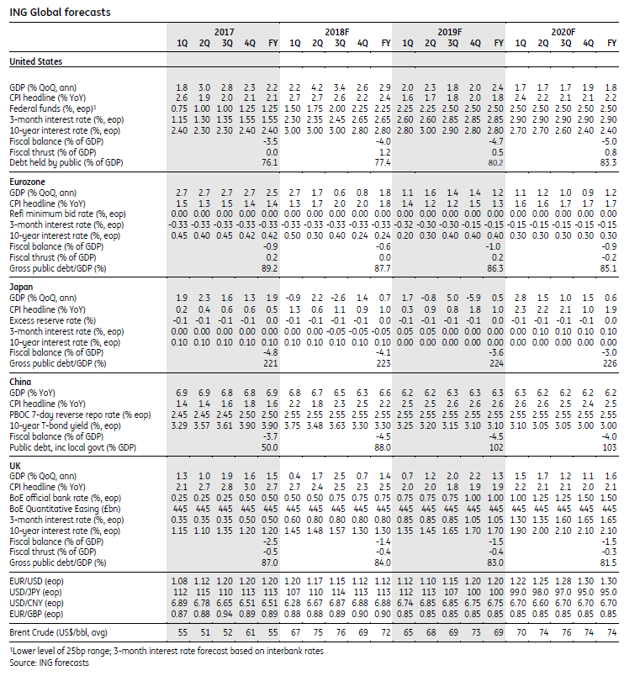

source: ING

content Disclaimer: This publication has been organized with the aid of ING fully for suggestions purposes regardless of a selected consumer's means, economic circumstance or funding goals. The suggestions doesn't represent funding recommendation, and nor is it investment, criminal or tax assistance or an offer or solicitation to purchase or promote any monetary instrument. study more

Editor's notice: The summary bullets for this article were chosen by searching for Alpha editors.

0 comentários:

Postar um comentário